TDS Accounting – Receipt v/s Accrual, which is better?

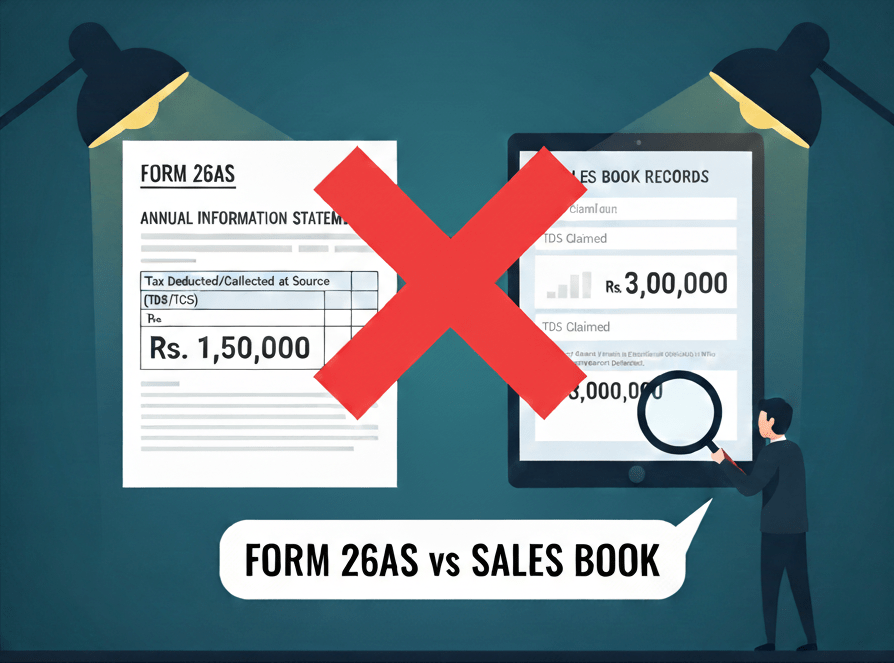

Companies follow different methods of TDS accounting – Accrual based v/s Receipt based accounting. With an objective to reconcile sales and TDS both with 26as form, which method is more suited?

Companies follow different methods of TDS accounting – Accrual based v/s Receipt based accounting. With an objective to reconcile sales and TDS both with 26as form, which method is more suited?

Explore possible reasons for Tax Credit mismatch with Form 26as, how to resolve them and best practices for 26as reconciliation with books

TaxReco’s Data Transformation Module can automate data cleaning and transformation activity, which is essential before TDS Payable reconciliation

Before closing the financial year, TDS Receivable and Payable data shall be audited to avoid surprises during the tax audit later

Issues faced in 26AS Reconciliation and their possible solutions using tax technology like TAN to PAN search

The concept of TDS was introduced with an aim to collect tax from the very source of income. As per this concept, a person/company (deductor) who is liable to make payment of specified nature to any other person/company (deductee) shall deduct tax at source and remit the same into the account of the Central Government

Clause 34 of Tax Audit Report (Form 3CD) requires Tax Auditors to comment on the overall Tax Deducted at Source (TDS/TCS) compliances by the tax payers. In accordance with the guidelines issued by Institute of Chartered Accountants of India on this clause, the auditors ask for a reconciliation of Financial Statements with the TDS/TCS returns.

#financetransformation “Transformation is the key” #taxautomation #taxtechnology

We read this often on social media and many companies have successfully transformed the way their finance department functions and are reaping the benefits of transformation viz.

01 July 2022 marked another important date for the TDS provisions. It marked the introduction of new sections under the TDS chapter of the Income Tax, 1961. It remains in line with the directive of the government to bring more and more accountability and transparency in the economy. This time the government targeted new areas of the TDS application.

The recon of the 34A is probably the most crucial recon of the Form 3CD.

Usually, companies take the data as filled out in the TDS returns filed during the year and submit the same with the details from all the quarters.